advertisement

In early 2023, U.S. consumer debt hit $16.51 trillion. This huge number shows how important loans are for American families. Borrowers often choose between secured and unsecured loans. Each type has its own benefits and drawbacks.

Let’s explore secured and unsecured loans in detail. We’ll look at their main features and common types. We’ll also compare the key differences between them.

This guide will help you choose the best loan for your needs. You’ll learn how to make a smart decision based on your finances.

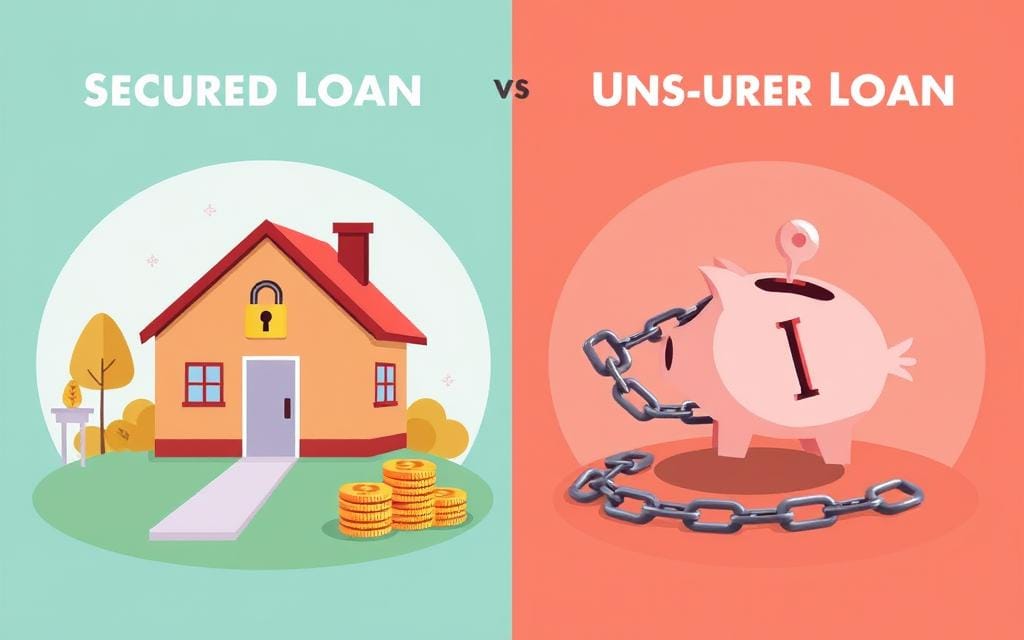

Understanding Secured Loans

Secured loans are backed by collateral, offering a guarantee to lenders. This collateral, like a home or car, can be seized if payments aren’t made. These loans are popular among individuals and businesses.

What Are Secured Loans?

Secured loans require borrowers to pledge an asset as collateral. This can be a house, vehicle, or investment accounts. The collateral’s value determines the loan amount and interest rate.

Common Types of Secured Loans

- Mortgages: Loans used to purchase or refinance a home, with the home itself serving as the collateral.

- Auto Loans: Loans used to finance the purchase of a vehicle, with the vehicle being the collateral.

- Home Equity Loans: Loans that use the borrower’s home equity as collateral.

- Secured Personal Loans: Loans that are secured by the borrower’s assets, such as a savings account or investment portfolio.

How Secured Loans Work

To get a secured loan, borrowers provide collateral to the lender. The lender assesses the collateral’s value to set the loan amount and interest rate.

If payments aren’t made, the lender can seize and sell the collateral. This helps them recover the loan balance.

Secured loans offer larger amounts and lower rates to borrowers. However, using collateral comes with risks. It’s crucial to weigh these risks before taking out a secured loan.

Understanding Unsecured Loans

Unsecured loans don’t require collateral and rely on the borrower’s creditworthiness. They offer a way to access funds without risking personal assets. These loans are popular for their convenience and flexibility.

What Are Unsecured Loans?

Unsecured loans are financing without collateral backing. Lenders evaluate credit scores, income, and debt-to-income ratios to assess default risk. These loans often have higher interest rates due to increased lender risk.

Common Types of Unsecured Loans

The most common types of unsecured loans include:

- Personal Loans – These loans can be used for a variety of purposes, such as debt consolidation, home improvements, or unexpected expenses.

- Credit Cards – Credit cards are a revolving form of unsecured credit that allows borrowers to make purchases and carry a balance from month to month.

- Student Loans – Federal and private student loans are unsecured loans used to finance higher education expenses.

- Business Loans – Small businesses may obtain unsecured loans to fund operations, expansion, or working capital needs.

How Unsecured Loans Work

Lenders assess borrowers’ creditworthiness to determine loan amounts and interest rates. They consider credit scores, income, employment history, and debt-to-income ratios. Unsecured loans typically have higher rates due to increased lender risk.

Borrowers must provide personal and financial information when applying. This includes credit scores, income details, and debt obligations. Lenders review this data to make approval decisions and set loan terms.

Key Differences Between Secured and Unsecured Loans

Secured and unsecured loans offer different options for borrowers. Knowing their differences helps you choose the right loan for your needs. Let’s explore the main features of each loan type.

Collateral Requirements

Secured loans need an asset as collateral. This could be a home or car. Unsecured loans don’t require any collateral.

Collateral reduces the lender’s risk in secured loans. This affects other loan features too.

Interest Rates Comparison

Secured loans usually have lower interest rates. The collateral makes them less risky for lenders. Unsecured loans come with higher interest rates.

Lenders charge more for unsecured loans to cover their higher risk.

Loan Amounts and Terms

Secured loans often offer higher borrowing limits. They also have longer loan repayment terms. The collateral gives lenders more security.

Unsecured loans typically have lower borrowing limits. Their loan repayment terms are usually shorter too.

| Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral | Required | Not required |

| Interest Rates | Lower | Higher |

| Loan Amounts | Higher | Lower |

| Loan Terms | Longer | Shorter |

These differences help you choose the right loan. Consider your financial situation and goals. Think about loan interest rates and loan repayment terms that work best for you.

Advantages of Secured Loans

Secured loans offer several benefits for borrowers. These advantages can help people make smart choices about their loan eligibility criteria.

Lower Interest Rates

Secured loans typically come with lower interest rates. Lenders see them as less risky because they’re backed by collateral. This allows them to offer better rates to borrowers.

Higher Borrowing Limits

With secured loans, you can often borrow more money. The collateral acts as a guarantee for the lender. This enables borrowers to access larger amounts for their financial needs.

Better Approval Rates

Secured loans usually have higher approval rates than unsecured ones. Collateral reduces the lender’s risk. This makes them more likely to approve applications, even for those with imperfect credit.

| Advantage | Explanation |

|---|---|

| Lower Interest Rates | Secured loans offer lower interest rates due to the reduced risk for the lender. |

| Higher Borrowing Limits | Secured loans allow borrowers to access larger loan amounts, as the collateral serves as a guarantee. |

| Better Approval Rates | Secured loans have higher approval rates, as the collateral reduces the lender’s risk. |

Knowing these key benefits helps borrowers choose the right loan type. It allows them to better assess their loan eligibility criteria. This knowledge can guide them in meeting their financial goals.

Disadvantages of Secured Loans

Secured loans offer benefits but have drawbacks too. Knowing these disadvantages is key to making smart loan decisions.

Risk of Losing Assets

The main risk of secured loans is losing your assets if you can’t repay. Your home or car serves as collateral for the loan. If you default, the lender can take and sell your property.

This can cause major financial and emotional stress. It’s crucial to consider this risk before taking a secured loan.

Lengthy Approval Process

Secured loans often take longer to approve than unsecured ones. Lenders must check the collateral’s value and your credit history carefully. This process can delay getting your funds.

If you need money quickly, a secured loan might not be the best choice.

Fees and Costs

Secured loans often come with extra fees. These may include appraisal, title search, and loan origination fees. These costs can add up fast, reducing potential savings from lower interest rates.

Always read the fine print. Understand all costs before signing a loan agreement.

Secured loans can be helpful, but they have risks. Consider both pros and cons carefully. Your decision should match your financial goals and risk comfort level.

Advantages of Unsecured Loans

Unsecured loans offer unique benefits for personal financing. They provide a flexible and accessible funding option without requiring collateral. This makes them attractive to many borrowers.

No Asset Risk

Unsecured loans don’t put your possessions at risk. You won’t lose your home or car if you can’t make payments. This gives borrowers peace of mind and a sense of security.

Faster Approval Process

Lenders can approve unsecured loans more quickly. There’s no need to assess collateral value or eligibility. This speeds up the application and approval process.

Fast approval is great for those needing urgent funds. It also helps borrowers who must secure financing quickly.

Flexibility in Usage

Unsecured loans offer more freedom in how you use the money. You can spend it on various personal expenses. These might include debt consolidation, home improvements, or unexpected medical bills.

This versatility is valuable for borrowers with diverse financial needs. It allows them to address multiple financial concerns with a single loan.

Unsecured loans have clear advantages for personal financing. They offer no asset risk, faster approval, and flexible usage. These features make them ideal for those seeking loan pre-approval and personalized financial solutions.

Disadvantages of Unsecured Loans

Unsecured loans don’t require collateral but have drawbacks. Knowing these can help you make smart financial choices. Let’s explore the potential downsides of unsecured loans.

Higher Interest Rates

Unsecured loans often have higher interest rates. Lenders see them as riskier and charge more to offset this risk. This makes unsecured loans costlier for borrowers.

The increased rates result in higher overall borrowing costs. Consequently, unsecured loans may be less appealing for those seeking affordable financing options.

Lower Borrowing Limits

Unsecured loans typically offer lower borrowing limits than secured ones. Lenders are cautious about lending large sums without collateral. This can be a problem for those needing substantial funding.

Stricter loan eligibility criteria

Lenders use stricter loan eligibility criteria for unsecured loans. They may require better credit scores and higher incomes. This can make the application process more challenging.

The tougher requirements can limit access to unsecured financing options. Not everyone will qualify for these loans.

| Unsecured Loan Disadvantages | Explanation |

|---|---|

| Higher Interest Rates | Lenders charge higher rates to offset the lack of collateral, resulting in a higher overall cost of borrowing. |

| Lower Borrowing Limits | Lenders are more cautious about extending large sums without collateral, limiting the maximum loan amounts available. |

| Stricter Loan Eligibility Criteria | Borrowers may need to meet stronger financial qualifications to be approved for an unsecured loan. |

Consider these drawbacks when thinking about unsecured loans. They can help you decide if this financing suits your needs. Weigh the pros and cons carefully before making your choice.

Loan Comparison: Secured vs. Unsecured

Choosing between secured and unsecured loans is a big decision. Understanding their differences can help you pick the right one for your needs.

Your choice will impact your financial goals. Let’s explore the key factors that set these loan types apart.

Factors to Consider When Comparing

Several important factors come into play when comparing secured and unsecured loans:

- Collateral requirements: Secured loans require you to put up an asset, such as your home or car, as collateral, while unsecured loans do not.

- Interest rates: Secured loans typically offer lower interest rates compared to unsecured loans due to the reduced risk for the lender.

- Loan amounts and terms: Secured loans generally allow for higher borrowing limits and longer repayment periods, whereas unsecured loans have lower limits and shorter terms.

Tools and Resources for Loan Comparison

Loan comparison calculators are helpful tools for comparing secured and unsecured loan options. These calculators let you input your financial information and compare different loan types side-by-side.

This makes it easier to find the best fit for your needs. You can see costs, terms, and features at a glance.

“Comparing loan options can be a daunting task, but with the right tools and resources, you can make an informed decision that sets you up for financial success.”

Financial advisors and lenders can also help you explore suitable loan options. They can discuss your specific situation and provide personalized advice.

When to Consider Secured Loans

Secured loans can be a smart choice in certain situations. They offer benefits that may outweigh potential drawbacks. Understanding when to choose a secured loan helps you make wise financial decisions.

Ideal Situations for Secured Loans

Secured loans use loan collateral as security. They’re great for large purchases or debt consolidation. These loans often have lower interest rates and higher borrowing limits.

They work well for financing homes or cars. If you’re struggling with multiple high-interest debts, a secured loan can help. It can streamline payments and potentially reduce overall interest costs.

Financial Health Considerations

- Before choosing a secured loan, assess your financial health and long-term goals. Consider your credit score, income stability, and ability to repay.

- Ensure the benefits align with your specific financial needs and objectives. Lower interest rates and higher borrowing limits should match your situation.

- Carefully evaluate the risks involved. Weigh the potential loss of assets against the advantages a secured loan may provide.

Evaluate your financial situation and specific circumstances carefully. This will help you make an informed decision. Choose a loan that aligns with your long-term financial well-being.

When to Consider Unsecured Loans

Unsecured loans offer flexibility for short-term or personal expenses. They don’t require collateral, making them suitable for various financial needs.

These loans are ideal for addressing unexpected costs or temporary cash flow issues. They can also help simplify repayment by consolidating existing debts.

Ideal Situations for Unsecured Loans

Unsecured loans can be beneficial in the following scenarios:

- Covering small personal expenses, such as unexpected medical bills, car repairs, or home improvements, where the loan amount is relatively low.

- Consolidating existing unsecured loans or debt consolidation loans to simplify repayment and potentially reduce interest rates.

- Financing short-term financial needs, such as a temporary cash flow shortage or a one-time purchase, where you don’t require a large loan amount.

Financial Health Considerations

Before getting an unsecured loan, assess your financial health and creditworthiness. Consider these key factors:

- Credit score: Lenders typically require a good credit score to qualify for an unsecured loan with favorable terms.

- Debt-to-income ratio: Lenders will assess your ability to make loan repayments based on your current income and existing debt obligations.

- Repayment capacity: Ensure that you have a reliable source of income and the financial means to make the monthly unsecured loan payments on time.

Evaluate your finances carefully before choosing an unsecured loan. This will help you make a decision that fits your financial goals.

Making an Informed Decision

Choosing between secured and unsecured loans is a critical financial decision. It’s vital to weigh your options carefully. Your choice can impact your finances for years to come.

Assessing Your Financial Situation

Start by evaluating your current financial standing. Look at your income, debts, credit score, and financial goals. This will help you find the best loan for your needs.

Calculate your debt-to-income ratio by analyzing monthly income and expenses. Check your credit report and score to understand your creditworthiness. Define your short-term and long-term financial objectives.

- Analyze your monthly income and expenses to understand your debt-to-income ratio.

- Review your credit report and score to gauge your creditworthiness.

- Determine your short-term and long-term financial objectives.

Consulting Financial Advisors

Seeking guidance from a professional financial advisor is a smart move. They can offer valuable insights based on their expertise in loan comparison and loan application process.

“A financial advisor can help you navigate the complexities of secured and unsecured loans, ensuring you make the most informed decision for your unique financial circumstances.”

A financial advisor can explain the pros and cons of each loan type. They might also suggest alternative financing options that better fit your needs.

Take time to evaluate all factors before deciding on a loan type. Consult a trusted financial professional for guidance. This approach will help you make a choice aligned with your financial goals.

Conclusion

Secured and unsecured loans have distinct advantages and disadvantages. Secured loans offer lower interest rates but risk asset loss. Unsecured loans provide quick approvals but have higher rates.

Mortgages and auto loans are examples of secured loans. They allow higher borrowing limits. Personal loans and credit cards are unsecured options with more flexibility.

Summary of Pros and Cons

Secured loans are more affordable but need collateral. The approval process can be lengthy. Unsecured loans are convenient and don’t risk assets.

However, unsecured loans can be more expensive. They also have lower loan amounts and stricter repayment terms.

Final Thoughts on Loan Choices

Consider your financial situation when choosing between loan types. Think about your long-term goals and risk tolerance. Understand the details of each loan option.

Weigh the factors of secured loans, unsecured loans, and loan comparison. This will help you make an informed decision. Choose the loan that best fits your financial needs.

FAQ

What are the key differences between secured and unsecured loans?

Secured loans require collateral, offering lower interest rates and higher borrowing limits. Unsecured loans don’t need collateral but have higher rates and lower limits. Approval processes differ too, with secured loans often having better approval rates.

What are the advantages of secured loans?

Secured loans offer lower interest rates and higher borrowing limits. They also have better approval rates. Lenders face less risk due to collateral, allowing more favorable terms for borrowers.

What are the disadvantages of secured loans?

Secured loans risk asset loss if you default. The approval process can be lengthy. There may be additional fees and costs to consider.

What are the advantages of unsecured loans?

Unsecured loans don’t put your assets at risk. They have a faster approval process. You have more flexibility in using the loan funds.

What are the disadvantages of unsecured loans?

Unsecured loans have higher interest rates and lower borrowing limits. They also have stricter qualification criteria. Lenders face more risk, resulting in less favorable terms for borrowers.

When should I consider a secured loan?

Consider secured loans for large purchases like homes or cars. They’re also good for consolidating high-interest debt. Lower rates and higher limits make them suitable for these financial needs.

When should I consider an unsecured loan?

Unsecured loans work well for smaller, short-term financial needs. They’re good for unexpected expenses or personal purchases. Quick approval and flexible usage make them ideal for these situations.

How can I compare secured and unsecured loan options?

Compare interest rates, loan amounts, repayment terms, and associated fees. Use loan comparison calculators to help you decide. Consult financial advisors to make informed choices based on your situation.